The realm of travel credit cards can be complex. Providers offer incredible benefits, and although they aren’t outright deceiving, they often lack clarity regarding the steps you must take. This is further complicated by the ever-changing loyalty environment, which makes it challenging to determine which cards are suitable for different individuals.

I’ve been traveling the world non-stop for the past seven years, moving through nearly 60 countries on a monthly basis. You might think that this kind of lifestyle would result in a massive airline bill. However, I discoveredtop methods to leverage credit card rewards for free travel, accumulating up to $10,000 in savings annually in certain situations. These savings aren’t due to chance. I have gained a deep understanding of nearly every credit card available, seeing each as a resource designed to help reduce my expenses. I also manage a biweekly points and miles newsletter with more than 1 million subscribers, have written hundreds of articles on this topic, and created my own course to help others achieve the same.

Not everyone desires to be like me, though. I carry up to eight credit cards in my wallet at any given time — far more than the typical person. But which one is ideal if you only want a single card? The answer is complex, and realistically, one card is unlikely to transform your life. Everyone has unique habits and objectives, and each card serves different purposes. However, if I were to rank some of the most popular cards available based on easy access to value and the highest likelihood of getting you free flights, this is how I would order them.

Read more: How to Pack a Single Carry-On for a Seven-Day Trip

1. The Capital One Venture X Rewards Credit Card

At the summit is theCapital One Venture X Rewards Credit Card. It has been my top suggestion for the last three years, and even with some modifications to its features, it remains an outstanding product. It distinguishes itself by choosing simplicity, making it ideal as a single-card system leader. If you have higher goals, it’s also remarkable when used as part of a larger plan.

One reason it’s highly beneficial is the flat-rate of 2 miles per dollar on all purchases. Unlike many other providers that focus on particular spending categories, Capital One cardholders don’t need to worry about anything. For instance, if you spend $2,000 each month, you can expect to earn approximately 48,000 miles annually, without much additional consideration. That’smore than enoughTo travel to Europe and return using a carrier such as KLM, Air France, Virgin, or Iberia. In technical terms, this could even be enough for a business class ticket with Virgin, depending on your travel dates. Additionally, if you spend $4,000 within the first three months of opening the card, you’ll earn 75,000 bonus miles. By the end of your first year, you could have around 123,000 miles. That’s an impressive beginning.

However, the income rate is simply this card getting started. At $395 per year to own, it’s not inexpensive, but it offsets that fee by offering a $300 travel statement credit annually for use on the Capital One travel portal, a bonus 10,000 miles on your cardholder anniversary, and a Priority Pass lounge membership (although its airport lounge policies are now much less accommodating) It’s a high-end card without the hassle and offers everyone a genuine opportunity to earn free travel. In terms of value, it’s the top card available.

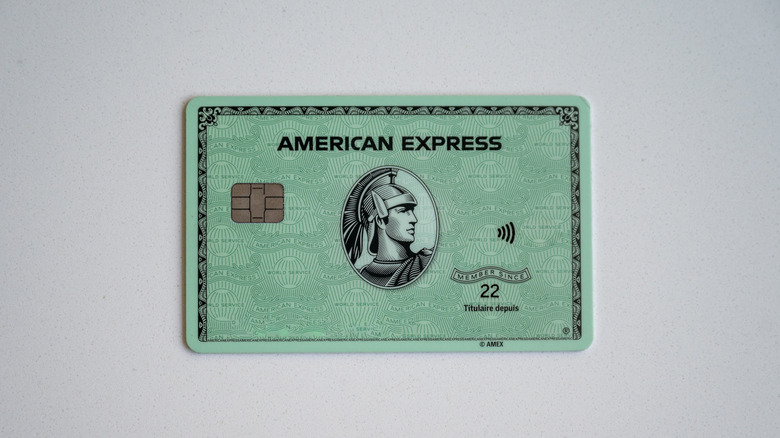

2. Amex Green Card

The Amex Greenflies under the radar in comparison to its more luxurious premium counterparts such as the Amex Gold and Platinum cards. However, those who possess the Green card are well aware of its impressive earning potential. In sharp contrast to the Venture X, there are minimal perks available, but theGreen is among the top credit cards designed for frequent travelers.

The headline earning rates provide 3x points per dollar on travel, transportation, dining at restaurants globally, and takeout and delivery within the U.S. Now, if you’re a frequent traveler, those rates should be really appealing to you. The definition of travel and transportation is much broader than what other cards offer, allowing you to earn 3x points on nearly all aspects of a trip. For instance, while other cards may only consider travel as hotels, flights, and possibly major train trips, the Green card applies this rate to everything from tours and ferries to subways and campgrounds. I stayed almost exclusively in Airbnbs for six years and used the Green card to pay for them each time. It was my main source of regular points during that period.

Now, if you’re not someone who frequently travels or dines out, it might not seem as appealing. This is where the personal aspect of this list becomes relevant. However, since you’re reading this, it’s reasonable to assume you have an interest in traveling. It also offers a 40,000-point introductory bonus, which can be obtained by spending $3,000 within six months of opening the card. While it’s not a substantial bonus,40,000Highly valuable American Express points can be very beneficial.

3. Citi Strata Premier

Although it is a large company, Citi has often seemed to be in the shadow of bigger names such as Amex, Chase, and Capital One. The reason for this is unclear. It may be due to the issuer’s choice to not launch a genuine premium card until2025However, even today, it still appears to trail behind its rivals. This reputation means that its exceptional cards have never received as much attention as other options—and it’s a significant disadvantage for everyone else.

The Citi Strata PremierThe issuer’s mid-level option costs $95 annually, offering a 60,000-point welcome bonus after spending $4,000 within the first three months, along with a $100 hotel discount each year to offset the annual fee entirely. Additionally, the rewards structure includes 10x points per dollar spent on travel through Citi Travel and 3x points on air travel, hotels, dining, grocery stores, gas stations, and EV charging stations. The 3x points rate on gas, restaurants, and supermarkets could cover a typical person’s monthly expenses. If $2,000 in spending falls into these categories each month, that would result in approximately 72,000 points annually.

For those worrying if Citi’s transfer partnersare less powerful than the others, that’s definitely not true. Its lineup was already solid, but it has now become the only genuine transfer partner for American Airlines, giving it an advantage over companies like Amex and making ThankYou points extremely valuable. The Strata Premier went from being rarely used in my wallet to becoming my primary card overnight once I realized I had no reason to pass it up. Don’t make the same error.

4. Chase Sapphire Reserve

The Chase Sapphire Reserveis Chase’s top-tier option and includes an astonishing annual fee of $795. Don’t be mistaken, you need to be cautious with this card, or it could turn into a financial drain. Calculate your expenses and benefits to make sure you’re truly receiving worthwhile value.

But for those who are okay with the risk-to-reward balance, the Reserve offers a significant impact. It includes an impressive 125,000 point welcome bonus, which can be obtained by spending $6,000 within three months, a $300 annual travel credit, $500 in credits for stays through its hotel program, IHG One Rewards Elite Status, a Priority Pass Select membership, Global Entry and TSA PreCheck credits, and various lifestyle credits. That’s an extraordinary amount of value available. I estimate Chase Ultimate Rewards points at aroundtwo cents each, so the bonus alone is valued at least $2,500 in travel. The remaining benefits total approximately $3,000, making it possible to achieve a significant return.

Even if you’re a frequent traveler, the earnings rates are strong, offering 4x points per dollar on hotels and flights, along with 3x points per dollar on dining. However, it’s crucial to do the math. Ensure you can comfortably meet the sign-up bonus, evaluate your annual travel spending, and determine if the perks provide genuine value. After all, you’re not saving $120 on DoorDash if you never intended to use it in the first place.

5. Amex Gold

One of the more prominent siblings referenced from the Amex Green, theAmex Goldis a card designed for food lovers who have significant expenses on groceries and dining out. It is technically a mid-level card from Amex, but with an annual fee of $325, it’s not a spontaneous decision — you’ll still need to calculate the benefits. That being said, it can be a powerful tool for earning points.

The positive aspect is that its welcome bonus can be worth up to 100,000 points after spending $6,000 within six months of opening the account. That equates to nearly $2,000 in value according to my calculation and is definitely worth considering. However, once the bonus has been redeemed, what does the Gold card still provide? Fortunately, there’s a lot to offer. Although it doesn’t have many perks, especially when taking into account its annual fee, it provides 4x points per dollar on up to $50,000 a year spent at restaurants, 4x points per dollar on up to $25,000 on groceries, 3x points per dollar on flights booked directly, 2x points per dollar on prepaid hotels, and 1x point per dollar on all other purchases, giving you a wide range of options. TheA credit card also offers Global Entry credit., which can help you save money as well, if you typically pay for it.

As I’ve noted previously, I employ a multi-card approach to avoid receiving just 1 point per dollar on any purchase, but the Gold card has played a significant role in my strategy. I spend a considerable amount on dining out (we can discuss whether that’s wise or not), and it has generated tens of thousands of points annually for both me and my partner. However, if you’re looking for just one card and spend heavily on groceries and restaurants, this could be the option to consider.

6. Chase Sapphire Preferred Credit Card

I really like the Chase Sapphire Preferred. It’s a straightforward card, yet it can deliver significant benefits for the right individual. Its simplicity, powerful earning categories, and impressive introductory bonus make it an ideal starting point for newcomers to the points and miles world, and it consistently ranks high on my suggestions for them. It’s a card you may eventually outgrow, but for straightforward value, it’s an excellent choice.

For a $95 annual fee, the introductory bonus is impressive. New cardholders can earn 75,000 Ultimate Rewards points after spending $5,000 within three months of opening the card. I estimate that to be worth approximately$1,500when it comes to travel, using them effectively can be beneficial, but even just through the Chase Travel Portal, you can get at least $1,000. The points accumulation rate is 3x points for every dollar spent on dining (including qualifying takeout and delivery), and 2x points for every dollar spent on travel-related purchases. Additionally, there are a few special categories, such as 3x points per dollar on certain streaming services and online grocery shopping. There’s also a small $50 Chase Travel Hotel credit to further enhance the value.

The worth of this card lies in its initial value. It serves as the starting point for numerous rewards and miles, and I keep it in my wallet for many years — as do others. I use it along with my other cards, particularly when traveling overseas, where a more lucrative Amex card might not be accepted. However, if this is your first genuine travel card, you could certainly do much worse.

7. Amex Platinum

The Platinum Card offered by American Express is arguably the best-knownThe credit card that is widely recognized as the most famous in the world, and likely the most renowned. It established the benchmark as the first high-end card, and its name has remained, even as it grew less exclusive over time. This card is a subject of debate because, in my view and that of many professionals, it no longer holds the same value it once did. Its benefits are more like a collection of discounts, its rewards rates are not impressive, and it comes with a hefty price tag.

However, I have still added it to this list for several reasons. Firstly, the bonus is substantial. You can earn up to 175,000 points by spending $12,000 within six months of getting the card. It’s a significant spending target, but it also offers a considerable number of points. This is more than $3,000 in travel value when transferred to a top airline partner. Secondly, the benefits are definitely worthwhile. It provides the finest lounge access available on any card, along with various statement credits that can be applied to your daily life. However, the rewards rates aren’t very good.

I frequently caution my readers about this card. At $895 per year, it’s extremely costly. However, those who utilize it wisely love it, as it provides more genuine benefits than any other offering. Calculate the perks and advantages that are truly valuable to you, and compare them to the fee. If the total is higher, you’re in a good position to enjoy all the card’s benefits. If not, consider other options. If you’re seeking a high-end card,compare it to the Sapphire Reserve first, which I believe is a more superior overall card.

8. Hilton Aspire Card

The Hilton Aspireis a jointly branded hotel card that exclusively accumulates Hilton Honors points. All the other products discussed previously have been highly beneficial transferable general credit cards.Even Rick Steves believes using these cards is a smart way to save money while traveling.. Although this implies the Aspire has certain limitations, a powerful hotel credit card can offer significant benefits.

The Aspire is Hilton’s high-end choice and costs $550. It’s not inexpensive, but it provides significant value over the course of a year, making it a worthwhile investment. The simplest way to get your money’s worth is through the free annual stay reward. Every year, you can redeem this benefit for a stay at nearly any Hilton property. This could be a luxurious hotel in the Maldives priced at $3,000 or a Hampton Inn in Ohio. It should be clear which end of the spectrum you should focus on. You’ll also receive complimentary Diamond Status with Hilton Honors, which isone of the top five hotel programs that are genuinely valuableI have been a Diamond Member for more than ten years and have never experienced a failure in being upgraded at any hotel. I consistently enjoy complimentary breakfasts, access to the executive lounge, and a clear change in how employees treat me.

The bonus is also appealing. You can earn 150,000 Hilton Honors Bonus Points by spending $6,000 within six months of getting the card. These days, it’s hard to find more than two nights at a decent hotel with that bonus, but it still offers a potential savings of a few hundred dollars. However, the real reason I’ve kept this card in my wallet for years is its experiential value.

9. Hyatt World Credit Card

If you’ve ever gone through any of my newsletters, you’d understand that I frequently highlight the immense value of World of Hyatt. The loyalty program maintains one of the most favorable award charts in the industry, and it has managed to keep this system even as many others have abandoned it in favor of a dynamic pricing model.

If you possess any points-earning Chase cards or a Bilt card, you have the option to transfer your points to Hyatt, but otherwise, you’re stuck.Opening one of its cardsThe optimal approach to address this is. The personal card does not provide a points bonus, but it does offer up to five complimentary nights in a Category 1 through 4 hotel, following a $15,000 spending threshold within the initial six months of possession. You will still receive three if you only spend $5,000 within three months, which is still favorable. Earning $15,000 on the card will grant you at least 15,000 additional points, sufficient for five nights at a Category 1 hotel. As a standalone card, I wouldn’t necessarily suggest it. However, if your primary focus is on hotel stays, there isn’t another card I would prefer.

10. Southwest Rapid Rewards Credit Card

The last item on the list is theSouthwest Airlines Rapid Rewards Credit Card. Once more, this is a co-branded card and not a points transfer option, similar to many others. It has been included here for several specific reasons that make it beneficial for the occasional traveler.

Southwest’s program doesn’t provide exceptional value. It’s difficult to get more than approximately 1.4 cents per point, which is lower compared to other programs that could offer 2, 3, or even 8 cents per point for premium class travel. However, what stands out is its dependability. Although you won’t exceed that 1.4 cent threshold, it’s also uncommon to fall significantly below it. Additionally, you have the ability to reserve any seat on the flight, rather than competing for just four award seats as with other airlines. This card provides a reliable boost of points that can be used when it’s most beneficial.

I usually suggest that individuals keep their Rapid Rewards Points and utilize them for last-minute domestic trips or as a final option when other premium airlines fail to meet your needs. It’s quite dependent on the situation, but they can be incredibly helpful when the timing is appropriate.

11. Methodology

For the past six years, I have been writing about and utilizing points and miles, which have helped us save nearly $10,000 annually between my partner and me while traveling the world full-time. I have ranked this list according to the ease of value for the average person, rather than following a strict “this card is better” approach. This is because each card comes with its own advantages and disadvantages, which can either help or hinder individuals based on their specific circumstances.

Eager to uncover more secret treasures and professional travel advice?Sign up for our free email newsletter and Add us as a preferred search providerfor entry to the world’s most closely guarded travel insights.

Read the original article on Islands.